Inflation Surprises Continue With PPI

Bulls failed to follow through after yesterday’s big move, but a cooler-than-expected inflation print helped hold onto the stock market’s gains. Let’s see what else you missed.

Today’s issue covers big-box retailer Target hitting its mark, Chinese stocks catching a bid, and two more tech titans reporting results.

Here’s today’s heat map:

9 of 11 sectors closed green. Consumer staples (+0.77%) led, & utilities (-0.31%) lagged.

U.S. producer prices experienced their largest monthly drop since April 2020, falling 0.5% in October. Its yearly increase of 1.3% was down from 2.2% in September, with core producer prices flat MoM. Meanwhile, manufacturing activity remains mixed, with the Empire State manufacturing survey showing modest growth during October.

Automakers remain in focus, with union workers at General Motors currently mixed in their votes on the proposed deal. In addition, Berkshire Hathaway’s 13-F filing showed that it sold its position in the stock, putting additional pressure on shares and investor sentiment.

Disney shares continued to rebound after catching a few analyst upgrades. Additionally, regulatory filings showed that activist investor ValueAct has been building a stake in the media conglomerate, believing its theme parks and consumer products businesses are alone worth low 80s per share.

Other symbols active on the streams: $NFLX(+2.96%), $NEGG (+30.80%)

Here are the closing prices:

| S&P 500 | 4,503 | +0.16% |

| Nasdaq | 14,104 | +0.07% |

| Russell 2000 | 1,801 | +0.16% |

| Dow Jones | 34,991 | +0.47% |

Chinese Stocks Catch A Bid

Chinese stocks have underperformed for several quarters as concerns about its slow economic recovery had investors looking elsewhere. However, after solid results from JD.com and better-than-expected economic data, traders are putting these stocks back on their radars.

Yesterday’s data showed that China’s industrial production and retail sales topped expectations in October, rising 7.6% and 4.6% YoY, respectively. Real estate remains a soft spot, with investment falling 9.3% YoY. With its government assessing new measures to bolster economic growth, the International Monetary Fund (IMF) recently raised its 2023 and 2024 growth forecasts.

Meanwhile, the e-commerce group JD.com showed signs of life in the third quarter. Its $0.92 per share in earnings and $34.2 billion in revenues topped analyst expectations. The consumer tech giant has been cutting costs to boost profitability in a slow sales environment, using lower prices and promotional activity to attract customers and buoy sales.

Below is a chart of popular Chinese internet ETF $KWEB perking up recently. It remains in a historic drawdown, over 70% below its 2021 highs. However, some traders and investors anticipate a trend change could occur if it breaks above the downtrend line from its late 2021 highs.

The recent improvements in price action and economic data have fund managers looking for opportunities among depressed mainland stock markets. Whether or not this turn in sentiment will stick remains to be seen. But for now, the market is back in focus on the long side.

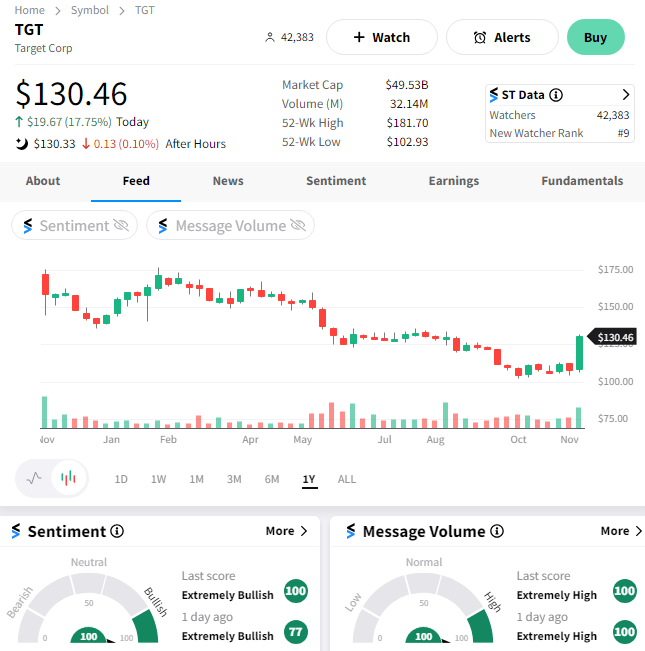

Target Hits Its Mark

The last twelve to eighteen months have been tough for retailers as consumers recovered from their pandemic-fueled shopping sprees. Some companies navigated this period better than others, with Targetbeing one that failed to adjust in a timely manner.

A range of issues pushed the stock lower, including poor inventory management, crime sprees hitting its stores, and a product mix that didn’t match customers’ expectations. Management’s inability to address these factors led to the stock’s largest drawdown since the great financial crisis.

However, the big-box retailer showed some signs of getting back on track when reporting third-quarter results. Its earnings per share of $2.10 on revenues of $25.4 billion topped the $1.48 and $25.24 billion anticipated by analysts.

With a slow sales environment, management’s efforts to address inventory and costs over the last year are finally paying dividends. Inventory levels fell 14% YoY while lower freight costs and other factors reduced the cost of goods sold. Gross margins expanded from 24.7% to 27.4%, while operating margins rose from 3.9% to 5.2%.

In regards to its revenue, overall comparable sales dropped 4.9%. Breaking that out, transaction volumes fell 4.1% YoY, and the average transaction amount fell 0.8% YoY. Additionally, store-based comparable sales fell 4.6% YoY, and digitally originated sales fell 6.0%.

Sales, general, and administrative (SG&A) expenses as a percentage of revenues rose to 20.9%, as the retailer relies more on promotional activity to drum up sales. Consumers continue to delay discretionary purchases, instead spending most of their funds on lower-margin necessities like grocery items.

As a result, management expects the holiday quarter to look similar, with a mid-single-digits YoY sales decline. Overall though, investors were happy to see the company get a handle on costs and place itself in a stronger position heading into 2024.

$TGT shares had their best day since August 2019, rising 18% to nearly 3-month highs. Our community is bullish on the turnaround story, with activity and sentiment readings sitting at extremes as the market closed.

We’ll get more information from Walmart tomorrow before the bell. But as of now, most retailers are providing cautious outlooks for the holiday quarter. The lower and middle-income consumer brackets remain challenged by inflation and falling savings levels. As a result, many expect this upcoming shopping season to be light, including FedEx, UPS, Home Depot, and now Target.

Recent U.S. economic data is also pointing towards that as well.

October retail sales recorded their first headline monthly decline since March, falling 0.1% MoM vs. expectations of 0.3%. Sales excluding auto and gas rose 0.1%, suggesting that consumers continued to spend despite concerns about inflation and the economy. Some analysts suggest October’s number is a sign of further weakness to come, given the third quarter’s pace of spending came in at “unsustainable levels.”

As always, there will be pockets of opportunity in the market. For example, off-price retailer TJX Companies. raised its full-year guidance for the third time this year and expects a robust holiday shopping season as consumers trade down to lower-priced options.

Time will tell, as it always does. We’ll keep you updated on the consensus view as more retail earnings roll in.

Tech Titans Continue Reporting

While investors are primarily focused on retailer earnings this week, they can’t escape the volatility that comes with tech earnings. Let’s quickly recap what we heard from two tech giants.

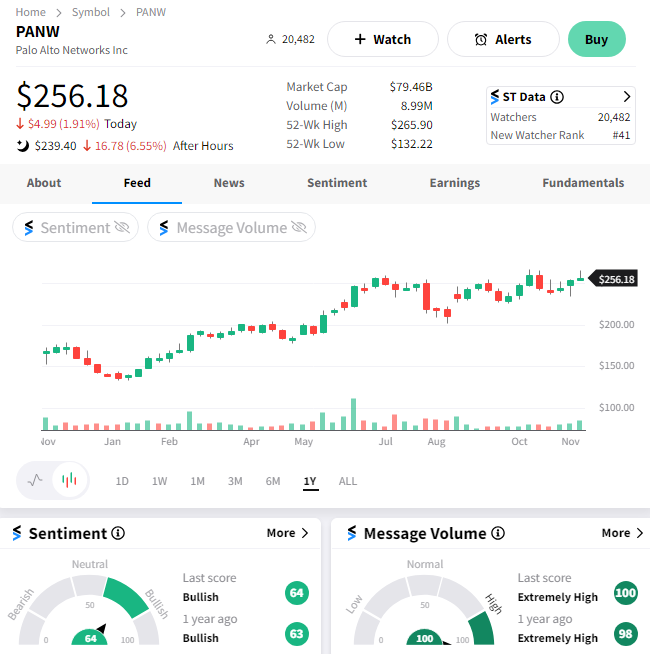

First up, cybersecurity firm Palo Alto Networks saw its first-quarter revenues jump 20% YoY to $1.88 billion. Meanwhile, adjusted earnings of $1.38 topped expectations of $1.16.

Executives say an unprecedented level of attacks is fueling strong demand in the cybersecurity market, but that higher cost of funds is offsetting or delaying some demand. As a result, its second-quarter billings guidance of $2.34-$2.39 billion fell short of the $2.43 billion consensus estimate.

$PANW shares continue their pullback from all-time highs, falling about 7% after the bell.

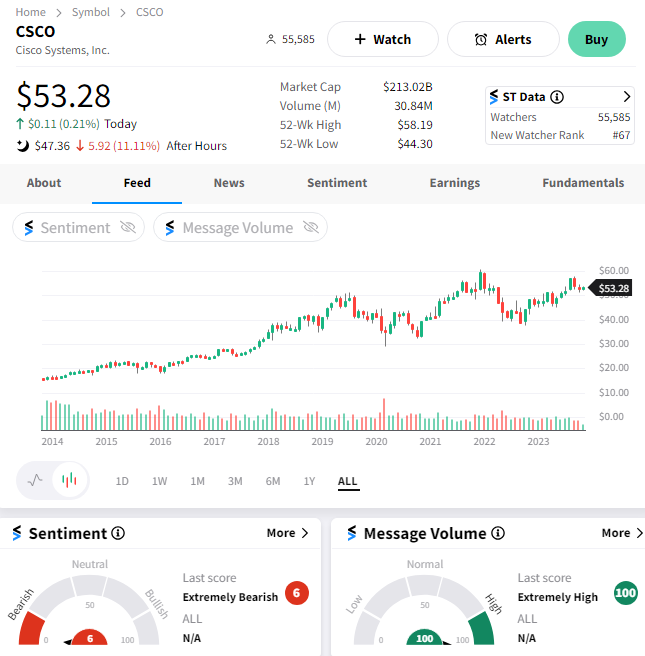

Networking, cloud, and cyber company Cisco also dropped after its guidance fell short of expectations.

The company’s adjusted earnings per share of $1.11 on $14.67 billion in revenues both topped estimates. Like other tech companies, Cisco raised its full-year earnings guidance but reduced its revenue guidance.

Executives said new product orders slowed during the quarter as clients worked to install and implement products ordered in the three previous quarters. They anticipate that one or two-quarters of shipped products are waiting to be implemented, which could reduce (or at least delay) future orders.

For now, Cisco remains focused on cost management to buoy earnings until demand rebounds. But the lackluster revenue guidance was enough to tick off investors, who are sending $CSCO shares down 11% after hours.

Bullets From The Day:

🚫 German regulator considers Ozempic export ban amid shortages. As Europe’s health systems grapple with the diabetes treatment shortage, driven primarily by its weight-loss benefits, the country is considering the export ban to allow supplies to catch up with demand. So far, the government has attempted to quell the number of “off-label” prescriptions by informing the public of the shortage and its impact on diabetes patients. However, if that proves ineffective, additional measures will likely be implemented. Reuters has more.

🤖 Forward Health launches a self-contained, AI-powered doctor’s office. The company started its journey to scale healthcare in 2017 by launching tech-forward doctor’s offices that replaced traditional medical staffing with technology solutions like body scanners, smart sensors, and algorithms that can diagnose ailments. It’s now taking that vision to the next level with “CarePod,” a portable artificial-intelligence-driven doctor’s office soon to be located in malls and offices, where users can get common tests and procedures done without a physician present for just $99/month. More from TechCrunch.

🎯 Microsoft takes on Nvidia by making custom AI chips. Recent rumors were confirmed today, with Microsoft unveiling its Azure Maia 100 and Cobalt 100 silicon chips designed and built for its cloud infrastructure. Microsoft began architecting its cloud hardware stack in 2017, putting it on the journey to develop its own custom chips to power its Azure data centers and prepare it for an artificial-intelligence-filled future. As for investors, they’ll have to assess whether this will eat into other chipmakers’ profitability or if demand is simply too high to matter. The Verge has more.

🎮 China’s ByteDance is the latest tech giant to back away from gaming. The TikTok owner is discussing the sale of its gaming unit Moonton Technology, just two years after it acquired the Shanghai-based studio in a $4 billion deal. At the time, ByteDance was flexing its commitment to become a major player in the $817 billion global video games market. With the acquisition’s performance not meeting expectations and competition growing in ByteDance’s other core businesses, the tech giant is the latest player to refocus its resources. More from Reuters.

📱 Meta looks to offload download oversight to the app stores and parents. The social media giant is supporting federal legislation that would require parental approval for app downloads for users under the age of 16. The company’s Global Head of Safety argues that parents should be responsible for approving their teen’s app downloads, citing a Pew Research study indicating that 81% of U.S. adults favored requiring parental consent for teens to create social media accounts. It comes as Meta faces lawsuits from a coalition of 42 states and D.C. that claim the company’s products are harmful to teens and young users. TechCrunch has more.